Europe Residential Storage 2026: HEMS Opportunities for Installers

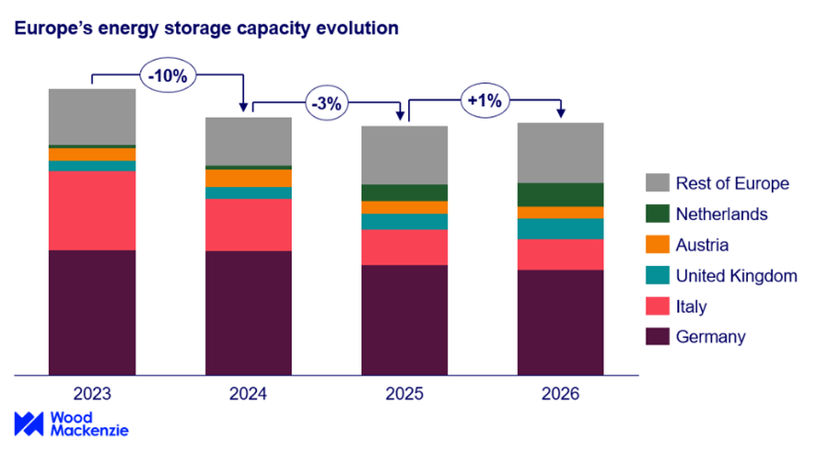

As we move through early 2026, you’ve probably already felt the shifts in the European residential battery storage market. Wood Mackenzie’s December 2025 report puts it clearly: installations dropped 10% in 2024 and another 3% in 2025—two consecutive years of contraction. The good news? The same analysts expect the market to stabilize in 2026 and start growing again meaningfully from 2027 onward.

Image source: Wood Mackenzie

Image source: Wood MackenzieChinese manufacturers now hold around 80% of the market (up from 68% in 2022), while European brands have fallen to roughly 12%. Despite this pressure, Europe still dominates seven of the world’s top ten residential storage markets. For you as an installer or distributor, this means real challenges: longer sales cycles, tougher price negotiations, and more customers putting projects on hold. But the fundamentals haven’t disappeared—residential PV keeps expanding, heat pumps and EVs are spreading, battery prices continue falling, dynamic tariffs are becoming common, and flexibility markets are opening up.

The question you’re likely asking right now is how to position yourself for the recovery. One of the strongest answers is moving beyond standalone batteries toward integrated solutions built around Home Energy Management Systems (HEMS).

Why the Market Plateaued — and What You’re Seeing on the Ground

The recent downturn wasn’t a surprise to most people in the trade. After the 2022–2023 energy price spike, electricity prices came down in many countries, making payback periods longer and self-consumption less urgent for some customers. Several key markets scaled back or ended generous storage subsidies, while grid feed-in tariffs stayed attractive in places. At the same time, Chinese suppliers used scale and cost advantages to win share aggressively, turning much of the market into a price battle.

You’ve likely experienced the consequences directly: customers comparing quotes more aggressively, projects delayed while they wait for better pricing, or even cancelled because the numbers no longer add up quickly enough. Selling on capacity and cycle life alone has become much harder when price is the main conversation.

2026 Outlook: Stabilization This Year, Growth from 2027

Wood Mackenzie sees 2026 as the turning point—volumes should stabilize, then begin climbing again in 2027 and beyond. The drivers are still there and, in many cases, getting stronger:

- Steady growth in rooftop solar across most European countries

- More households adding heat pumps and electric vehicles, pushing up electricity consumption

- Battery prices continuing to fall thanks to global manufacturing scale

- Wider rollout of time-of-use and dynamic pricing tariffs

- Increasing participation opportunities in virtual power plants and local flexibility markets

These factors are already starting to rebuild demand, especially where smart tariffs and grid services create real financial upside.

From Price Competition to Value Creation — Why HEMS Matters for You

As competition over basic battery hardware has intensified, European manufacturers have responded by focusing on higher-value, software-driven solutions. Wood Mackenzie points out a clear difference: 59% of European-branded systems come with Home Energy Management Systems, compared with only 22% of Chinese-branded ones. That gap isn’t accidental—it’s a deliberate move to shift the conversation from “cheapest kWh” to “lowest annual energy cost and best long-term return.”

HEMS platforms do exactly that. They monitor and intelligently control energy flows across your customers’ solar PV, battery, EV charger, heat pump, and household loads. The result? Higher self-consumption rates, better use of dynamic tariffs, participation in demand-response or VPP programs, and overall lower bills. For your customers, it means a stronger business case and faster payback. For you, it means a way to escape pure price competition: projects that include HEMS usually carry higher margins, happier clients, and more repeat or referral work.

At Ultimati Energie, our LiFePO4-based RESS systems—such as the RE-HA1 All-in-one residential energy storage solution—are built with this shift in mind. They support DC-coupled architectures, flexible high/low-voltage options, and integrated zero-export control, making them straightforward to pair with leading HEMS platforms. That lets you offer a complete, optimized energy management package instead of just another battery—helping protect your margins and strengthen your position when customers start asking for more than the lowest upfront cost.

Where the HEMS Opportunity Is Strongest

The recovery won’t happen evenly. Wood Mackenzie highlights several countries where HEMS potential stands out thanks to high distributed energy resource penetration, smart tariffs, and active flexibility markets:

- Germany — huge existing PV base, dynamic pricing, and growing VPP participation

- United Kingdom — strong EV uptake, smart meter rollout, and emerging local flexibility schemes

- Netherlands — fast solar growth, time-of-use tariffs, and early smart-home adoption

- Sweden — widespread heat pumps and EVs, cold-climate storage needs, and supportive policy signals

If you’re active in any of these regions—or planning to expand there—prioritizing HEMS-compatible hardware now will give you a real advantage when demand picks up.

Quick FAQ: European Residential Battery Storage Market 2026

When will the energy storage market start growing again?

Wood Mackenzie expects stabilization in 2026 and clear growth resuming in 2027, driven by PV expansion, electrification, and dynamic tariffs.

What exactly does HEMS do for my customers?

It optimizes energy use across solar, battery, EV, heat pump, and home loads—boosting self-consumption, cutting bills, and opening doors to VPP revenue.

How can I stand out when everyone is competing on price?

Shift toward integrated solutions with HEMS. Customers will pay more for lower lifetime costs and better performance, giving you healthier project margins.

Which countries look strongest for HEMS right now?

Germany, UK, Netherlands, and Sweden—high DER penetration, smart tariffs, and flexibility market development.

Final Thoughts

The European residential battery storage market is coming out of a tough plateau phase. While pure hardware competition remains fierce, the growing role of intelligent energy management is creating a clear way to differentiate and build lasting value.

If you’re reviewing your 2026 product lineup, thinking about adding HEMS capabilities, or just want to talk through how these trends might affect your next quarter’s pipeline, we’d be glad to chat. Whether you need technical alignment ideas, or a quick simulation of what a HEMS-integrated project could deliver for your customers, we’re here—no pressure, no obligation.

Feel free to reach out at https://en.u-energie.de/pages/contact-us.

Ultimati Energie Deutschland GmbH is a Germany-based B2B energy storage system provider specializing in scalable residential and C&I battery storage solutions for European partners.

Become a Partner

Sales: +49 1624886367

Customer Support:

+49 15226994869

Address: Ober der Röth 4, 65824 Schwalbach am Taunus, Germany

Copyright © 2026 Ultimati Energie Deutschland GmbH All rights reserved.